Contents:

If you’ve read through the investing glossary or the first part of the practical investing guide you may have a good understanding of some basic but important terms and ideas related to investing. You may also be asking, what next? All of this information is great but its utility without a practical application is limited to factoids to tell your friends and family about, a Rosetta Stone for the financial news on TV or online (still pretty useful), and maybe a winning answer in a game of Trivial Pursuit.

With these training wheels of knowledge, we can continue on the path to investing on our own by opening an investing account with an online brokerage or bank, adding funds to it, and placing our first trade.

Opening an Investing Account

Before we can buy or sell anything, we need to open an account with a brokerage or bank that has access to the funds we want to buy or the exchanges that we want to interact with. This process generally involves a few steps similar to opening a bank account:

- Completing forms with general information about you – name, address, contact info, SIN (accounts are tied to it for CRA reporting), employment status, etc.

- Completing more forms with banking account information – usually for the initial funding of the account and account linking for additional fund transfers

- Completing even more forms regarding your financial situation – current assets and liabilities (debts), investment knowledge, risk tolerance, etc. (referred to as Know Your Client)

- Providing proof of identification (driver’s license, passport, etc.)

- Choosing an investment account type

- Waiting a while for the process of verification and account creation to be complete

Types of Investing Accounts

There are two main types of accounts: taxable (non-registered) and non-taxable (registered). The difference as the names suggest is whether the money in the account is subject to investment income tax or not.

Non-taxable accounts are preferable when possible and include RRSP and TFSA varieties each with their own ability to defer tax or provide tax-free returns (everything about them outlined in this post applies).

Taxable accounts are “regular” accounts subject to investment income tax but carry the benefits of having no limit on deposits made to them (contribution limits apply to investment RRSP and TFSA accounts too) and possibly fewer forms/paperwork to fill out (no RRSP or TFSA registration process).

The account type you choose is dependent on your situation and whether you have contribution room in your RRSP or TFSA. You could open up several different accounts as well – a taxable one and a TFSA for example, but it’s your responsibility to keep track of any non-taxable account contributions and report investment income on your tax return in April (this is pretty easy as most, if not all, banks and brokerages provide electronic versions of the required tax forms that include the numbers from your account for the year).

Bank Route

Some banks sell funds of their own and make them available to clients for purchase through their existing online portals usually through some kind of mutual fund investing account (e.g. Scotiabank through their Scotia OnLine portal). This route is generally much quicker and simpler to setup if you are already a customer of the bank. It generally offers a much smaller subset of available funds to purchase (as compared to all of the listed stocks on an exchange) which can be easier to digest and choose from.

These can be taxable and non-taxable “bank-specific mutual fund” investing accounts but this strategy limits you to only being able to invest in a limited number of funds offered by the bank which most likely carry higher fees than doing it yourself with a brokerage (e.g. Scotia Global Balanced Fund with an MER of 2.01%).

An example of a bank-specific mutual fund investing account that I’ve used (and still have) is the one with Tangerine bank. They a few different funds in the form of their “core” (5 available) and “global ETF” (3 total) portfolios. The available portfolios in each set generally have the same holdings with the difference between them being the asset allocation.

Though they carry a higher MER than putting together your own portfolio with a brokerage account and have asset allocations and holdings that you can’t modify, they’re easy to purchase through the banking portal, carry no account setup or ongoing account fees, and have lower MERs than traditional mutual funds (0.77% - 1.06% vs 2% or more)1.

For simplicity and ease of use, the Tangerine funds/portfolios above might be worth the fee for some (it was for me in the beginning).

Brokerage Route

Going the brokerage route can be a little more involved (as outlined in the account opening steps above) but offers the greatest variety of investment options and the most control for someone looking to do it themselves online.

Many banks have a self-directed (DIY) online brokerage of their own like RBC Direct Investing, TD Direct Investing, and Scotia iTrade but the Internet has also allowed entirely online discount brokerages like Wealthsimple and Questrade to emerge.

They all provide the same service of allowing you to open taxable or non-taxable investment accounts and generally follow the same steps above with the benefit of most times being able to do it entirely online.

Fees

Fees are something you need to watch out for as they can hide in a lot of places. Trading fees (to buy from or sell on an exchange), account fees (opening, maintaining an account with limited assets, closing), transfer fees (moving money out of the account), and more are sometimes buried in web pages or documents but you still need to be aware of them.

Below is a small comparison of fees associated with some common investment account actions from a few of the brokerages listed above (current as of this post’s published date).

The general rule is that bank-owned brokerages charge more fees for more activities while online/discount ones don’t. This could be because it costs banks more to have physical locations and staff there to help customers invest in person, they have some kind of brand premium (perceived as more trustworthy), they charge fees because they can, online brokerages are absorbing similar fees, or all of the above.

Read the fees pages of any brokerage you’re thinking of using very carefully (including the legal fine print at the bottom of the page).

Funding the Account

This is a fairly easy and painless part of the process assuming the account has been opened. If a bank account was linked as part of the creation process in the beginning, then you can pretty easily initiate an electronic funds transfer (EFT) between it and the investment account although it may take a few days to process before it shows up for you to trade with.

Some brokerages also allow you to fund your investment account via a bill payment from your online bank – using the brokerage as the payee and your investment account number as the destination account.

Trading

The interface of each brokerage’s platform (website) will differ but they will all offer similar functionality around searching for specific stocks and funds, placing buy/sell orders, and reviewing your portfolio information (book value, market value, number of shares, etc.).

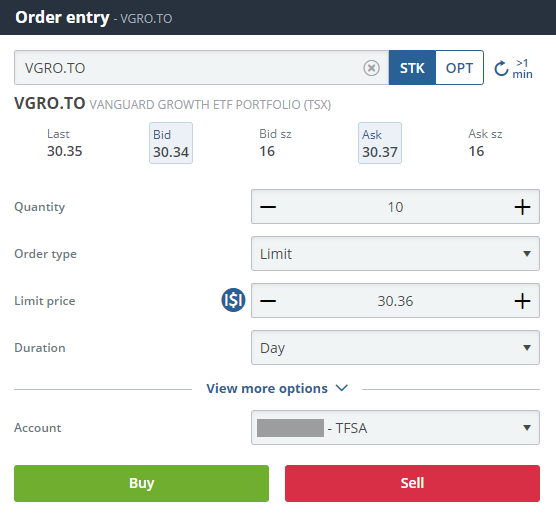

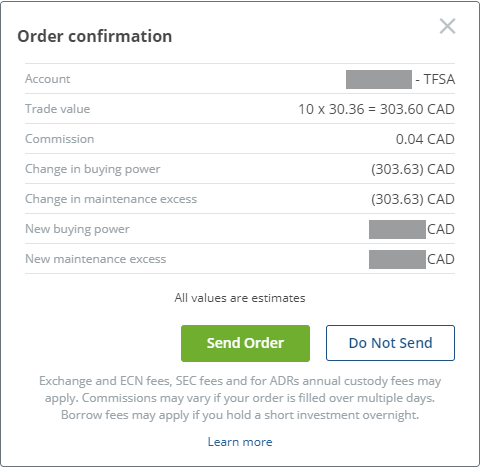

Below are a few screenshots showing the different trading interfaces of Questrade and Scotia iTrade2.

Questrade trade form:

Questrade trade confirmation:

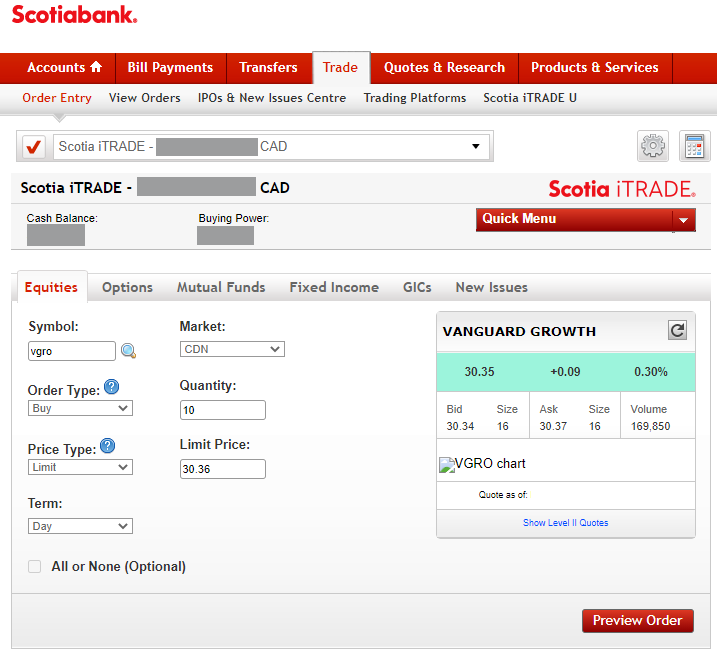

Scotia iTrade trade form:

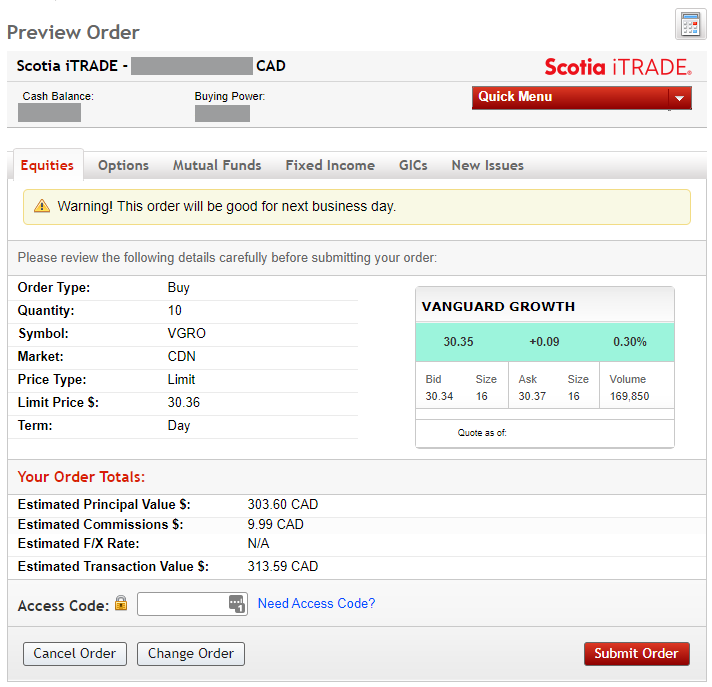

Scotia iTrade trade confirmation:

The trading process with any of the platforms will follow the same flow (shown in the above screenshots): decide on a stock/fund to purchase, enter its ticker name into a form with the number of shares you want to buy or sell, enter a price (if placing a limit order), and hit the order button.

Trading is fairly straightforward, figuring out what to trade and how much of it is more involved.

Tracking Your Portfolio’s Value

After the account has been opened, funded, and trades have been made within it, we can shift our attention to tracking our portfolio’s value.

Note: Tracking the value of your portfolio on a daily or even hourly basis can be tempting but also stressful as it will fluctuate up and down with the market. If it drops too low, some people may think about liquidating it and pulling out their money (for fear of losing more). This is what we want to avoid as it defeats the entire purpose of investing for the long term (which is what we’re doing if we’re using an RRSP and usually a TFSA as well). Knowing and investing according to your risk tolerance will help a bit (lower tolerance = less risky investments = smaller potential downturns) but we’re all humans in the end and it can be tough to stomach the drops. Out of sight, out of mind is the adage we generally want to aim for in these cases.

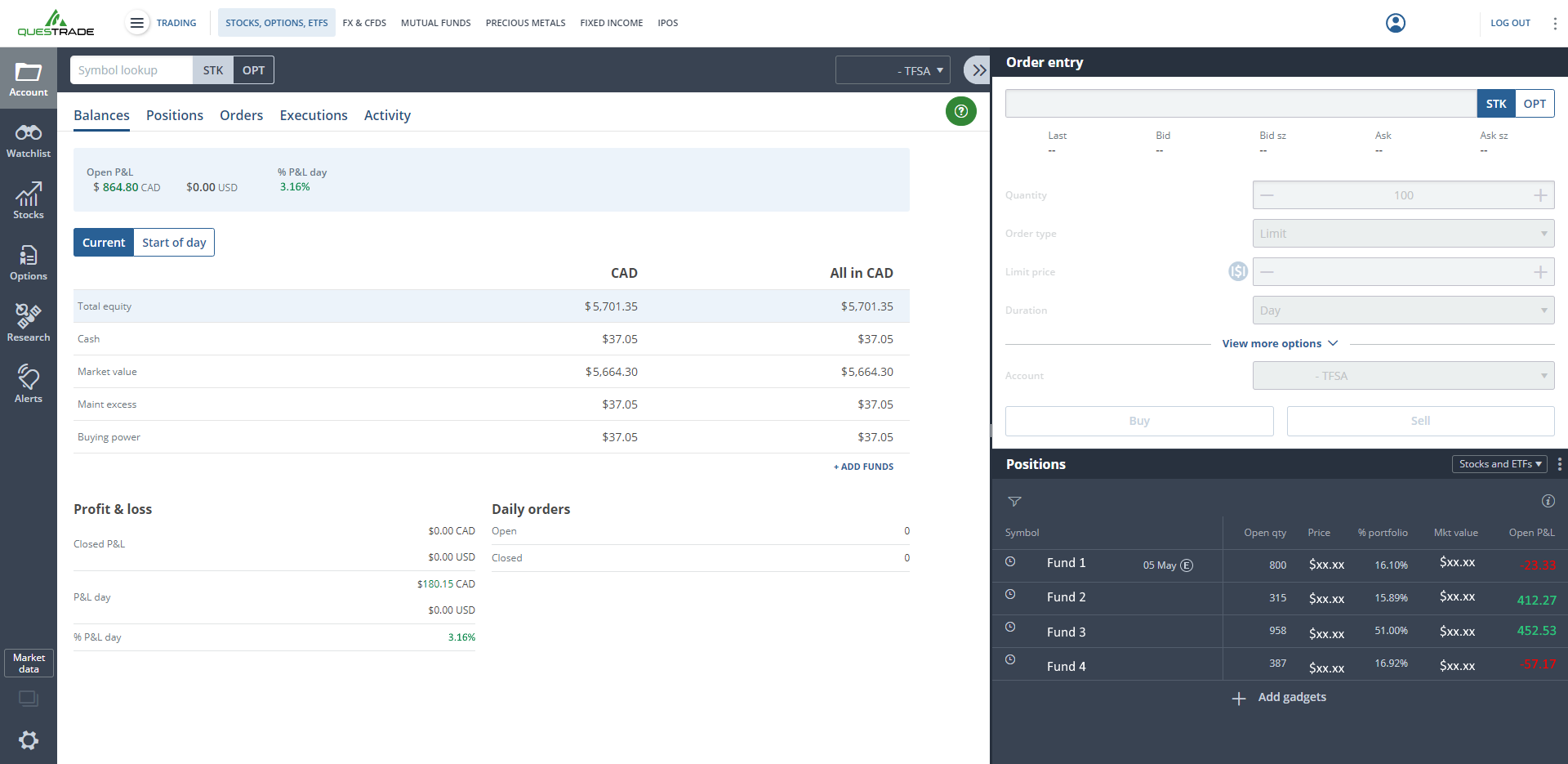

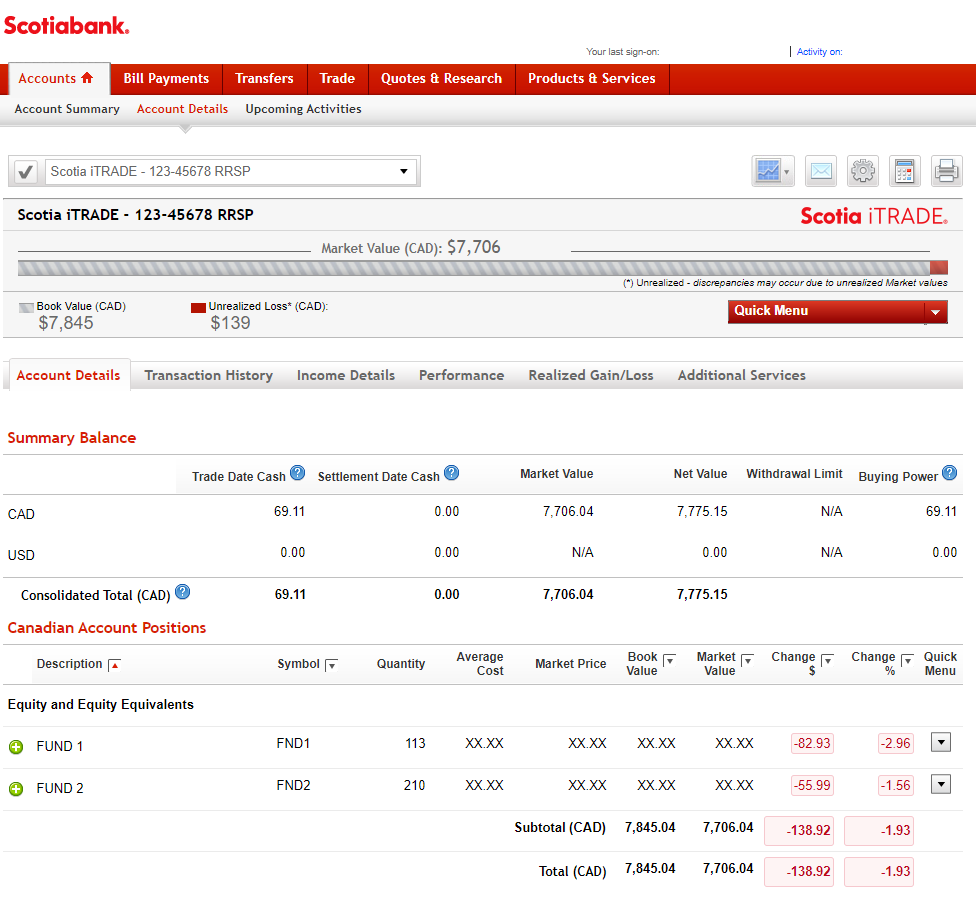

All of the platforms will display your portfolio’s value and most will break it down by each stock or fund – both with number of shares and total market values for them.

Questrade portfolio screen (click for larger image):

Scotia iTrade portfolio screen (click for larger image):

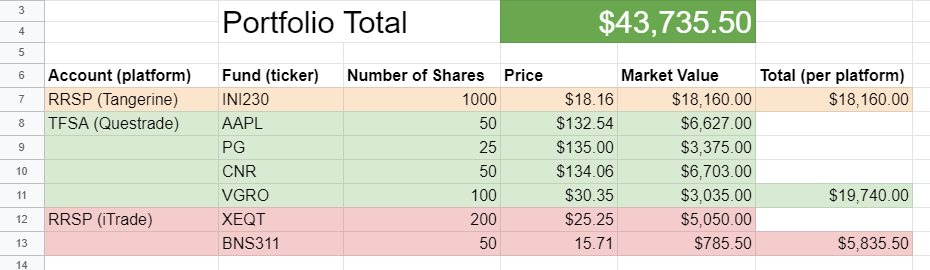

Google Sheets

If you have more than one platform you use for investing, don’t want to login to the platform to see your portfolio’s value, or want to have some kind of unified dashboard will all of your investments, then something like Google Sheets might be worthwhile to you.

Google Sheets is a web-based spreadsheet application similar to Microsoft Excel. I’ve been using it for years to track my budget and spending and recently starting using it to track my portfolio as well. It has a useful integration with Google Finance (Google’s site for tracking financial quotes, news, etc.) that can pull in real-time data of stocks and funds prices (for some – up to a 20 minute delay for others) on different exchanges.

With this we can create a sheet with a simple dashboard that lists all of our portfolio assets, their market prices, number of shares (that we can update manually whenever more are purchased), and market values calculated from that data.

Using Functions in Google Sheets

To use the Google Finance integration, we put the following function in whichever cell we want to place the price, replacing EXCHANGE_CODE with the exchange that contains the stock ticker you’re looking for (use this chart to find the code) and STOCK_TICKER with the actual ticker code (note that the quotation marks " and colon : below are part of the required format).

=GOOGLEFINANCE("EXCHANGE_CODE:STOCK_TICKER","price")

Some examples for Canadian and US stocks and ETFs:

=GOOGLEFINANCE("NASDAQ:AAPL","price")

=GOOGLEFINANCE("NYSE:PG","price")

=GOOGLEFINANCE("TSE:CNR","price")

=GOOGLEFINANCE("TSE:VGRO","price")

Some mutual funds don’t seem to work as expected with the GOOGLEFINANCE function like the Tangerine funds mentioned earlier. To get those prices we can use Morningstar (an investment research site) and another function in Google Sheets: IMPORTXML. This function takes a webpage in the XML format and retrieves the price from a specific element in that page.

To use it we replace FUND_TICKER in the function below with the ticker of the fund we’re looking for. If you find a fund on the Morningstar site like this,look at the URL and copy the value between the FundServCode= portion and the @ symbol (e.g. ...FundServCode=TDB900@... – TDB900 in this case).

=IMPORTXML("http://quotes.morningstar.com/fund/c-header?t=FUND_TICKER", "//span[@vkey='NAV']")

Some examples for Canadian mutual funds:

=IMPORTXML("http://quotes.morningstar.com/fund/c-header?t=INI230", "//span[@vkey='NAV']")

=IMPORTXML("http://quotes.morningstar.com/fund/c-header?t=TDB900", "//span[@vkey='NAV']")

=IMPORTXML("http://quotes.morningstar.com/fund/c-header?t=BNS311", "//span[@vkey='NAV']")

With these two functions, it’s possible to retrieve prices for probably most if not all of the stocks and funds we want to buy and track. If you’d like to experiment more, I’ve created an example Google Sheet (pictured below) with a basic dashboard that uses the functions above.

TL;DR

Opening an investing an account with a brokerage (or bank) is similar to opening a bank account – forms need to be filled out with your personal and financial information. They can be taxable (non-registered or “regular”) and non-taxable (registered like an RRSP and TFSA) accounts. Watch out for account fees (opening/closing accounts), trading fees (buying/selling shares), and other fees (wire transfer, withdrawing money).

Fund your account with an electronic funds transfer (EFT) or bill payment from your bank account. Submit trade orders on the platform by selecting a stock/fund with its stock ticker code, choose a quantity to buy or sell, decide on a limit (set min/max price to sell/buy) or market (current price of share on the market) price, and hit the order button.

View your portfolio value by logging into the platform but try not to check it everyday (fluctuations can be stressful). Bonus points: create a dashboard with a tool like Google Sheets to see all of your portfolio holdings and values at once.

-

Full disclosure: I first started investing with the Tangerine set of funds (the balanced growth “core portfolio” specifically) after doing some research (Canadian Couch Potato recommended them as an option when I started) and found them better than the mutual funds offered by the bank I used. I hadn’t read enough and wasn’t comfortable with direct investing yet so decided on them for the time being. I still hold the funds as part of my larger portfolio but also invest with a brokerage. I have no affiliation (marketing or otherwise) with Tangerine and have nothing to gain from recommending them. They fulfilled my criteria at the time and are still a viable middle ground between going full DIY with a brokerage and paying too much for actively managed mutual funds. ↩︎

-

Full disclosure: I use these platforms for my personal investments. I have no affiliation (marketing or otherwise) with either of them and have nothing to gain by discussing them. They work well for my needs and the screenshots are purely for your information. ↩︎

Categories

| personal-finance

Tags

| investing

| tfsa

| rrsp